Published: November 30, 2025

Chevron stock today: price, yield and performance snapshot

Chevron Corporation (NYSE: CVX) heads into the final month of 2025 looking fundamentally strong but still fighting a perception problem in the market.

As of the latest close on Friday, November 28, Chevron shares finished around $151.13, giving the company a market value of roughly $300–302 billion. [1]

That puts the stock about 10–11% below its 52‑week high of $168.96 and modestly above its recent lows near $132. [2] Over the past year, Chevron has lagged the S&P 500, even as broader U.S. equities have rallied, a point highlighted in new analysis from Barchart that explicitly frames CVX as an underperformer despite a recent bounce. [3]

Where Chevron does shine right now is income:

- Forward annual dividend: about $6.84 per share

- Dividend yield: roughly 4.5–4.6%, based on the current share price

- Payout schedule: $1.71 quarterly dividend; the most recent ex‑dividend date was November 18, 2025, with payment scheduled for December 10, 2025 [4]

Chevron has raised its dividend for 38 consecutive years, putting it firmly in dividend‑aristocrat territory. [5]

So on November 30, 2025, investors are looking at a mega‑cap energy stock with a high yield, record production and clear long‑term guidance — but a share price that’s still playing catch‑up to the wider market.

Q3 2025: record production, big cash flows and Hess integration

The current news flow around Chevron stock still starts with its third‑quarter 2025 results, released at the end of October. [6]

Key highlights:

- Reported earnings:$3.5 billion (or $1.82 per diluted share), down from $4.5 billion a year earlier

- Adjusted earnings:$3.6 billion ($1.85 per share)

- Record production:4.1 million barrels of oil equivalent per day (BOE/d), up 21% year‑on‑year, reflecting both organic growth and volumes from the Hess acquisition

- Cash flow from operations:$9.4 billion

- Adjusted free cash flow:$7.0 billion

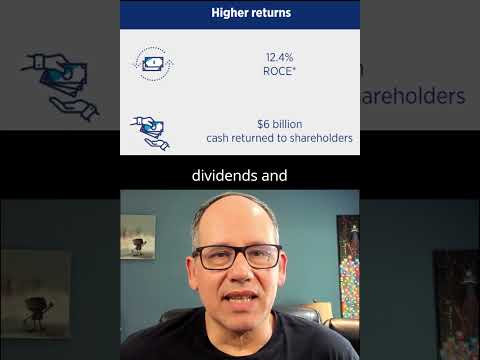

- Capital returns: around $6 billion returned to shareholders through dividends and buybacks in the quarter, and over $78 billion over the past three years [7]

The Hess deal, which finally closed in mid‑2025 after regulatory delays, weighed on reported earnings via severance charges and transaction costs, but it also boosted production and future growth options. Management described integration as “progressing well,” with synergies expected as Hess assets are folded into Chevron’s streamlined structure. [8]

The market initially liked what it saw: several outlets noted that CVX popped more than 3% immediately after the report as investors digested record output and robust free cash flow despite softer oil prices. [9]

Investor Day 2025: 10%+ free‑cash‑flow growth and a pivot to efficiency

On November 12, 2025, Chevron followed up earnings with an Investor Day that effectively reset the long‑term thesis for the stock. [10]

The company laid out a plan to 2030 built around three main pillars:

- Cash‑flow and earnings growth

- At a base case of $70 Brent crude, Chevron says it can grow both free cash flow and earnings per share by more than 10% annually through 2030. [11]

- Production is expected to rise 2–3% per year, from the current 4.1 million BOE/d, driven by the Permian, Gulf of Mexico, Hess assets and international projects. [12]

- Capital discipline and cost cuts

- Planned capital expenditure has been cut to a range of $18–21 billion per year, down from prior guidance of $19–22 billion. [13]

- Chevron increased its cost‑reduction target to $3–4 billion by the end of 2026, up from previous guidance, with much of the savings tied to restructuring and use of digital technologies to monitor and automate operations. [14]

- Management also stressed that the company expects to fund both capex and the dividend even if Brent falls toward $50 per barrel, signaling a “through‑the‑cycle” payout strategy rather than a boom‑and‑bust one. [15]

- New growth vectors, including AI‑linked power

- Chevron plans its first project to power an AI data center with natural gas in West Texas, targeting a final investment decision in early 2026 and start‑up by 2027. [16]

- The firm also aims to boost exploration spending by about 50%, focusing on the U.S. Gulf of Mexico, South America, West Africa and the Mediterranean, while pruning lower‑return assets. [17]

The Financial Times captured the mood neatly: rather than chasing sheer production growth, Chevron’s new plan explicitly prioritizes profits and free cash flow over barrels, leaning heavily on capex discipline and cost reduction. [18]

For Chevron stockholders, the message is: less empire‑building, more cash compounding.

Big exploration optionality: Namibia and Lukoil’s global assets

Two stories from mid‑November add some high‑upside (and high‑uncertainty) seasoning to the Chevron narrative.

Namibia’s Mopane discovery

Reuters reports that Chevron and TotalEnergies have emerged as front‑runners to acquire a 40% operating stake in Galp’s Mopane oil field in Namibia, a discovery estimated to hold at least 10 billion barrels of resources. Galp expects to select a winning bidder by year‑end. [19]

Namibia currently has no producing oil fields, but a string of discoveries since 2022 has analysts projecting that the country could become a top‑15 oil producer by 2035. [20] Chevron already has acreage nearby in the Orange Basin; its first wells there were non‑commercial, but they helped de‑risk the geology. [21]

A Mopane stake would give Chevron a multi‑billion‑barrel, long‑dated growth option that fits its 2030+ production story—albeit with significant technical, political and environmental risk.

Eyeing Lukoil’s overseas portfolio

In a separate Reuters scoop, Chevron is reported to be studying options to buy parts of sanctioned Russian major Lukoil’s international assets, alongside Exxon Mobil and private‑equity suitors. [22]

The portfolio under discussion includes:

- Stakes in Kazakhstan’s Tengiz and Karachaganak fields, where Chevron is already a partner

- Potential interest in Iraq’s West Qurna 2, one of Lukoil’s crown‑jewel projects

- Downstream and retail assets in Europe and elsewhere

The U.S. Treasury has given companies a time‑limited window—through December 13, 2025—to negotiate with Lukoil, so any Chevron move here would likely come quickly or not at all. [23]

Both the Namibia and Lukoil storylines underscore a key point for CVX stock: even while it preaches capital discipline, Chevron is still hunting for big, long‑life barrels.

Venezuela, geopolitics and near‑term volatility

Another November headline that matters for Chevron stock revolves around Venezuela.

Bloomberg reporting cited by several outlets says Venezuela turned to a Chevron‑booked tanker to secure critical refinery feedstock after U.S. authorities blocked a Russian vessel, spotlighting Chevron’s unique position as a U.S.‑authorized operator in the country. [24]

That episode came just months after the temporary U.S. license allowing Chevron’s expanded Venezuelan operations was allowed to lapse, reducing some high‑margin production that had helped support earnings earlier in 2025. [25]

For shareholders, the message is: Venezuela is both an opportunity and a policy risk. Chevron retains relationships and infrastructure that could be very valuable if sanctions ease further—but changes in U.S. foreign policy can quickly swing volumes and margins.

Dividends, buybacks and the “bond‑like” part of the story

Numbers first:

- Forward dividend yield: ≈ 4.5%

- Annual dividend per share:$6.84

- Dividend growth: around 4–5% over the past year, with decades of uninterrupted increases [26]

- Buyback yield: estimates hover around 2–4%, for a total shareholder yield (dividends + repurchases) in the 6–9% range. [27]

This high, growing payout is exactly why Chevron has been popping up in recent dividend‑investor pieces:

- Benzinga highlighted CVX as one of three energy stocks with dividend yields above 4% backed by solid free cash flow and generally positive analyst ratings. [28]

- Multiple Motley Fool articles include Chevron among top high‑yield stocks to buy and hold through at least 2030, emphasizing the 2030 cash‑flow guidance and Hess‑driven production growth. [29]

For investors who treat large, stable dividend payers as “equity bonds” with upside, Chevron’s current valuation—double‑digit upside to consensus targets and a mid‑4% yield—looks appealing.

Analyst and options market sentiment: cautiously bullish, with dissent

Across Wall Street, the consensus view on CVX remains constructive:

- A compilation of 40 analyst views puts the median 12‑month price target around $171, versus the current ~$151 share price, implying roughly 13% upside. [30]

- The highest target, from Mizuho, is $204, about 35% above current levels; Mizuho maintains an “Outperform” rating and recently nudged that target up from $191 following Investor Day. [31]

- UBS reiterated a Buy rating and a $197 price target, pointing to improved capital discipline, production growth and free‑cash‑flow visibility through 2030. [32]

Consensus ratings across these firms cluster around “Moderate Buy” to “Outperform.” [33]

But not everyone is cheering:

- Zacks Research recently downgraded Chevron to “Strong Sell”, reflecting concerns about downward‑revised earnings estimates and near‑term weakness in crude prices. [34]

- Zacks also named Chevron its “Bear of the Day” earlier this week, highlighting that earnings are likely to be lower than in the 2022–2023 boom even as the company absorbs Hess‑related costs. [35]

Meanwhile, the options market has seen a string of unusually large trades skewed slightly bullish, according to recent Benzinga flow analysis—suggesting that some institutional players are positioning for a rebound while hedging downside risk. [36]

In short: analysts mostly like Chevron, but the enthusiasm is tempered by commodity‑price uncertainty and integration risk.

What big money is doing: Norges Bank moves in, others reshuffle

The latest batch of 13F filings and institutional‑ownership news adds more color to Chevron’s shareholder base:

- Norges Bank, Norway’s sovereign wealth fund, disclosed a new position of about 19 million Chevron shares, worth approximately $2.7 billion, giving it roughly 1.1% of the company. [37]

- A long list of U.S. wealth managers and pension funds have been tweaking their positions. Recent filings show:

- Some firms trimming stakes (e.g., New York State Common Retirement Fund cutting its holdings by about 6.6%; various RIAs halving their exposure). [38]

- Others adding or initiating positions (Quadrant Capital Group, Pursue Wealth Partners, and multiple regional advisors building positions ranging from a few thousand to tens of thousands of shares). [39]

Net‑net, the picture looks less like a stampede in either direction and more like active portfolio rotation within a stock that remains heavily owned by institutions and index funds.

Why the stock has struggled anyway

If Chevron is pumping record volumes, paying a fat dividend and promising 10% annual cash‑flow growth, why isn’t the stock ripping?

Recent commentary and data highlight a few headwinds:

- Underperformance vs the S&P 500: Barchart pegs CVX as about 11–12% below its 52‑week high, with the stock down over the last three months while the S&P 500 has gained more than 5%. [40]

- Oil price softness: Brent and WTI have spent much of 2025 below 2022–2023 peaks, pressuring upstream earnings even as volumes rise. [41]

- Venezuelan license uncertainty: The lapse of Chevron’s broader Venezuelan license in May reduced some high‑margin barrels just as the company was absorbing Hess‑related costs. [42]

- Restructuring and layoffs: Chevron is cutting 15–20% of its workforce—roughly 6,000–8,000 jobs—as part of a push to improve cash generation. That should boost margins over time, but it adds near‑term restructuring charges and operational risk. [43]

Add in macro factors—questions about global oil demand growth, OPEC+ supply decisions and energy‑transition policy—and it’s not surprising that investors have demanded a risk premium before bidding CVX back toward its highs.

Is Chevron (CVX) stock a buy on November 30, 2025?

From today’s vantage point, the investment case for Chevron stock looks something like this:

What the bulls see

- High, growing income: ~4.5% dividend yield with a four‑decade growth record, plus ongoing buybacks. [44]

- Clear long‑term roadmap: Management is explicitly targeting >10% annual growth in free cash flow and EPS through 2030 at moderate oil prices, with the math laid out in detail. [45]

- Optionality: Namibia’s Mopane, Lukoil’s global assets and expanded LNG and Gulf of Mexico projects give Chevron multiple ways to grow beyond its base plan. [46]

- Valuation support: The stock trades with double‑digit upside to Wall Street’s median price target, even after Friday’s bounce. [47]

What the bears worry about

- Commodity‑price risk: If oil stays weak or falls, the 10% growth plan becomes harder to deliver, even with cost cuts. [48]

- Execution risk on Hess and new projects: Integration stumbles or cost overruns in Namibia or Lukoil assets could erode returns. [49]

- Policy and legal overhangs: Sanctions dynamics in Venezuela and ongoing climate‑related lawsuits remain wildcards for long‑term cash flows. [50]

- Conflicting signals from research shops: Strong‑Sell calls from Zacks clash with bullish targets from Mizuho and UBS, underscoring that the range of outcomes is wide. [51]

For Google News readers, the practical takeaway is simple: Chevron is no longer the pure oil‑price rocket it was during the post‑pandemic boom. It’s evolving into a cash‑flow‑focused, high‑yield compounder that still carries all the usual upstream and geopolitical risks.

Anyone eyeing CVX today needs to decide whether they’re comfortable owning a volatile energy business in exchange for a big, growing stream of cash and potential upside if management delivers on its 2030 playbook.

References

1. www.investing.com, 2. www.barchart.com, 3. www.barchart.com, 4. stockanalysis.com, 5. stockanalysis.com, 6. www.nasdaq.com, 7. www.keyfactsenergy.com, 8. www.keyfactsenergy.com, 9. coincentral.com, 10. www.reuters.com, 11. www.reuters.com, 12. www.reuters.com, 13. www.reuters.com, 14. www.reuters.com, 15. www.reuters.com, 16. www.reuters.com, 17. www.reuters.com, 18. www.ft.com, 19. www.reuters.com, 20. www.reuters.com, 21. africanenergycouncil.org, 22. www.reuters.com, 23. www.reuters.com, 24. seekingalpha.com, 25. markets.financialcontent.com, 26. stockanalysis.com, 27. stockanalysis.com, 28. www.benzinga.com, 29. stockanalysis.com, 30. tickernerd.com, 31. www.gurufocus.com, 32. finance.yahoo.com, 33. tickernerd.com, 34. www.marketbeat.com, 35. www.zacks.com, 36. stockanalysis.com, 37. www.marketbeat.com, 38. www.marketbeat.com, 39. www.marketbeat.com, 40. markets.financialcontent.com, 41. www.nasdaq.com, 42. markets.financialcontent.com, 43. www.barrons.com, 44. stockanalysis.com, 45. www.reuters.com, 46. brazilenergyinsight.com, 47. tickernerd.com, 48. www.nasdaq.com, 49. www.keyfactsenergy.com, 50. seekingalpha.com, 51. www.marketbeat.com

Stock After Hours: What Happened on Dec. 19, 2025—and What to Watch Before the Next Market Open")

Stock After Hours on Dec. 19, 2025: Google Cloud’s Multibillion-Dollar Deal, CyberArk Regulatory Update, and What to Watch Before the Next Market Open")

Stock After Hours Dec. 19, 2025: MSCI Index Risk, Bitcoin Rebound, and What to Watch Before the Next Market Open")

: $816M Space Force Satellite Deal Fuels a Friday Surge — What to Know Before the Next Market Open")

Stock After Hours on Dec. 19, 2025: Price Moves, Deal Headlines, Analyst Forecasts, and What to Watch Before the Next Market Open")

Stock on November 30, 2025: Options Surge, Dividend Hike and Value Push Shape Investor Sentiment")