Chevron Corporation (NYSE: CVX) is back on the radar for global investors on December 2, 2025, as markets digest a major analyst upgrade, fresh offshore exploration deals in Nigeria, and new geopolitical risk after a drone attack on a key export pipeline — all against the backdrop of Chevron’s ambitious 2030 cash‑flow growth plan.

This article pulls together the most important news, forecasts and analysis as of December 2, 2025, to help you understand where Chevron stock stands right now and what could drive CVX next.

Note: This article is informational and not investment advice. Always do your own research or consult a licensed financial adviser before investing.

Chevron stock price today: CVX dips but stays positive year‑to‑date

As of late trading on December 2, 2025, Chevron stock trades around $149.77, down roughly 1.8% on the day, after an intraday range between $149.33 and $152.87.

According to recent institutional data, Chevron shares sit roughly in the middle of their 12‑month trading band, with a low near $132.04 and a high around $168.96. [1]

On a performance basis:

- Year‑to‑date (YTD), CVX is up around 9–10%, depending on the data provider. [2]

- Over the past 12 months, total returns are roughly flat to slightly negative (around –1% to –2%), meaning Chevron has lagged the S&P 500, which is up in the mid‑teens percentage range over the same period. [3]

In other words, Chevron has been a modest winner in 2025, but not a market leader — and most of the story has come from its dividend and capital‑return profile rather than explosive share price gains.

Fresh Wall Street sentiment: HSBC upgrade, UBS target and mixed consensus

HSBC: Hold → Buy, with a higher price target

On December 1, 2025, HSBC upgraded Chevron from “Hold” to “Buy” and raised its price target from $166 to $169. The bank’s analyst Kim Fustier highlighted improving cash‑flow visibility after the Hess acquisition and Chevron’s disciplined capital spending. [4]

That new target implies roughly 13% upside from around $150, before counting Chevron’s 4–5% dividend yield.

UBS: reiterating Buy with a more aggressive target

Separately, UBS reiterated a “Buy” rating on Chevron with a price target of $197, underscoring a more bullish view than the broader Street. [5]

If that more optimistic forecast plays out, it suggests potential upside of around 30% from current levels (again, before dividends).

What the broader analyst community says

Consensus snapshots today show a nuanced, but generally constructive, picture:

- StockAnalysis.com reports that 16 analysts currently rate CVX, with an average rating of “Buy” and a 12‑month price target of $172.13, implying roughly 13–15% upside from the current share price. [6]

- MarketBeat, which aggregates a wider range of brokers, shows a more cautious average rating of “Hold”, with 11 Buy, 8 Hold and 4 Sell ratings and a consensus target around $166.16. [7]

- A detailed roundup from TS2 Tech notes that most major target ranges cluster in the mid‑$160s to mid‑$170s, with outliers both higher and lower — consistent with a moderate upside, moderate‑risk profile. TS2 Tech

In short, Wall Street sentiment has turned more positive in the very near term, thanks to the HSBC upgrade and supportive notes from UBS and others, but not all analysts are convinced. There is still a material minority of “Sell” and cautious “Hold” ratings.

New Nigeria deal: Chevron deepens offshore exploration with TotalEnergies

One of the biggest fresh headlines for Chevron this week is a high‑profile offshore Nigeria farm‑out deal.

On December 1, 2025, TotalEnergies announced it will sell a 40% stake in two offshore exploration licenses in Nigeria — PPL 2000 and PPL 2001 in the West Delta basin — to Star Deep Water Petroleum, a Chevron subsidiary. [8]

Key points:

- After the deal, TotalEnergies keeps 40% and remains operator, Chevron holds 40%, and South Atlantic Petroleum (SAPETRO) retains 20%. [9]

- The two blocks sit in Nigeria’s West Delta basin and cover roughly 2,000 square kilometres, a sizeable exploration footprint in a mature but still resource‑rich province. [10]

- The farm‑out builds on a June 2025 swap, where TotalEnergies acquired a 25% stake in 40 offshore U.S. leases operated by Chevron in the Gulf of Mexico. [11]

For Chevron, the Nigeria move:

- Shares early‑stage exploration risk with a major partner experienced in West African deepwater.

- Potentially adds long‑dated barrels that could support its 2030 production and cash‑flow targets.

- Signals that Chevron is still willing to invest in conventional offshore oil, even as it talks more about lower‑carbon projects and AI‑related power demand.

Zacks and other equity research outlets framed the transaction as a way for Chevron and TotalEnergies to “de‑risk and develop new opportunities” in Nigeria, while cementing a global exploration partnership spanning the Gulf of Mexico and West Africa. [12]

CPC drone attack: geopolitical risk meets Chevron’s Kazakh growth engine

Perhaps the most dramatic risk factor in the last few days has been a Ukrainian naval drone attack on the Caspian Pipeline Consortium (CPC) terminal at Novorossiysk in Russia — the main export route for Chevron‑led production in Kazakhstan.

What happened at the CPC terminal?

- Over the weekend, a Ukrainian drone strike damaged one of CPC’s three single‑point moorings (SPM‑2) at the Black Sea terminal, temporarily halting loadings and forcing tankers to leave the area. [13]

- Chevron confirmed to Reuters that crude loadings from its Tengizchevroil venture are still continuing, using another mooring (SPM‑1), even as repairs are underway. [14]

- As of December 2, 2025, CPC is racing to return SPM‑3 from maintenance to active service within about a week, far earlier than its original two‑month schedule, to restore full capacity. Right now, with only one mooring in operation, exports are running at just over half normal levels. [15]

The CPC pipeline handles more than 1% of global oil supply, transporting crude from Kazakhstan’s giant fields — Tengiz, Kashagan and Karachaganak — plus some Russian barrels. [16]

Chevron leads Tengizchevroil (TCO), which has been undergoing a $48 billion expansion, pushing Kazakhstan’s output to record highs earlier this year. [17]

Why it matters for CVX

- The attack underlines geopolitical risk around one of Chevron’s core growth hubs.

- Even though exports have resumed at reduced capacity, any further damage to CPC or extended outage would directly hit Chevron’s volumes and cash flow.

- Analysts quoted by TS2 Tech and other outlets note that the CPC incident is a live reminder that Chevron’s free‑cash‑flow story is tightly linked to politically sensitive infrastructure. TS2 Tech+1

For now, the market seems reassured that exports are still flowing, but the headline risk remains high, and future flare‑ups could inject volatility into CVX.

Hess acquisition: massive growth platform – and real integration costs

In July 2025, Chevron closed its long‑running acquisition of Hess Corporation, after winning a high‑profile arbitration battle against Exxon Mobil and CNOOC over Hess’s Guyana assets. [18]

Key elements of the deal:

- The transaction, valued at roughly $53–55 billion, gives Chevron a 30% stake in Guyana’s Stabroek Block, which contains more than 11 billion barrels of discovered recoverable resources. [19]

- Hess also brings 463,000 net acres in the Bakken (North Dakota) and other U.S. assets, expanding Chevron’s shale footprint. [20]

In the third quarter of 2025, Chevron reported that the newly acquired Hess assets contributed an expected 450,000–500,000 barrels of oil equivalent per day (boe/d), helping push company‑wide production to a record 4.1 million boe/d, up 21% year over year. [21]

However, the integration isn’t painless:

- Chevron said it expected to take a $200–400 million hit in Q3 related to the Hess deal, largely from severance and transaction costs. [22]

- The company is cutting more than 100 oil‑industry jobs in North Dakota, with filings showing 111 Hess‑related layoffs in Minot and Tioga starting in late September. [23]

For investors, Hess is a double‑edged story: it turbocharges Chevron’s growth profile in Guyana and the Bakken, but also adds execution risk, restructuring costs and social/political scrutiny.

Q3 2025 results: record production, softer profits but an earnings beat

On October 31, 2025, Chevron released its third‑quarter 2025 results. The headlines:

- Reported earnings:$3.5 billion, or $1.82 per diluted share, versus $4.5 billion ($2.48 per share) in Q3 2024. [24]

- Adjusted earnings: about $3.6 billion, or $1.85 per share, beating consensus estimates around $1.71. [25]

- Revenue: just under $49.7 billion, ahead of analyst expectations near $47.0 billion. [26]

- Production: a record 4.1 million boe/d, 21% higher than a year earlier, thanks in large part to Hess volumes. [27]

- Cash flow from operations:$9.4 billion, with adjusted free cash flow of $7.0 billion. [28]

Margins remain decent but not spectacular:

- MarketBeat’s recap notes a net margin of about 7.0% and return on equity near 9.9% in the quarter. [29]

- Revenue was actually down about 1.9% year‑on‑year, highlighting the drag from lower average oil prices even as volumes hit records. [30]

Bottom line: Chevron beat earnings expectations in Q3, thanks to production growth and refining margins, but absolute profits are still lower than last year, and the company is leaning heavily on integration synergies and cost cuts to support its long‑term story.

2030 roadmap: double‑digit cash‑flow growth, capex discipline and AI‑powered energy

At its Investor Day on November 12, 2025, Chevron laid out an updated long‑term plan that has become central to analyst forecasts. [31]

Key elements of the 2030 roadmap:

- Free cash flow growth: Targeting more than 10% annual growth in free cash flow through 2030, assuming Brent at $70 a barrel. [32]

- Production growth: Planning for 2–3% average annual oil and gas production growth, leveraging Guyana, the Permian, Tengiz and new exploration such as the Nigeria blocks. [33]

- Cost cuts: Increasing its cost‑reduction goal to $3–4 billion by end‑2026, up from a prior $2–3 billion target, partly via technology, remote operations and asset sales. [34]

- Capex discipline: Lowering annual capital expenditure guidance to $18–21 billion, while still funding key growth projects and lower‑carbon investments. [35]

- Breakeven resilience: Management says Chevron can cover capital spending and dividends at Brent prices below $50 per barrel, giving the company room to operate through cycles. [36]

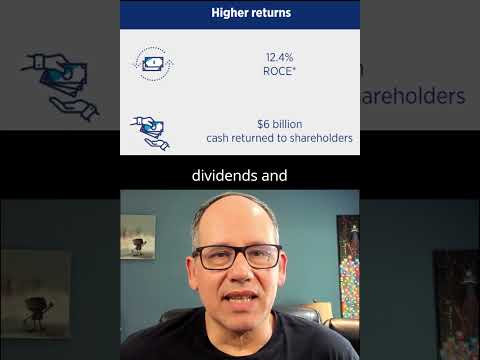

- Shareholder returns: From 2026 onward, Chevron is targeting $10–20 billion a year in share buybacks, depending on commodity prices, on top of its dividend. [37]

One interesting newer angle: Chevron is pivoting into supplying power for AI data centers, including a planned gas‑fired, AI‑optimized data center in West Texas targeted for 2027, a project it says could marry natural gas demand with digital infrastructure growth. [38]

Management’s view on oil prices: cautious through 2026

Against that bullish long‑term backdrop, Chevron’s own finance chief is striking a cautious note on near‑term oil prices.

In a recent interview covered by Energy Reporters, CFO Eimear Bonner warned that the current oil‑price slump could persist into 2026, citing:

- Strong production from OPEC+ and non‑aligned producers.

- Additional supply growth from Guyana, Brazil, Canada and U.S. shale.

- A market still digesting high inventories and muted demand growth. [39]

Energy Reporters and related analysis argue that while supply growth is likely to slow by late 2026, giving room for a possible price recovery, the next 12–18 months may remain choppy — a direct headwind to Chevron’s earnings momentum. [40]

This is a crucial context for any Chevron stock forecast: the company’s 2030 targets look achievable on paper, but the path between 2025 and 2027 could be bumpy if oil stays under pressure.

Dividend, yield and payout: Chevron as an income stock

For many investors, Chevron is first and foremost a dividend story.

Current dividend profile

Recent data from several sources show:

- Quarterly dividend:$1.71 per share, implying an annualized $6.84. [41]

- Forward yield: About 4.5–4.6% at current prices. [42]

- Payout ratio: Roughly 95–96% of current earnings, but closer to 89% of free cash flow, meaning dividends are tight on accounting profit but better covered by cash. [43]

- Track record: Chevron is widely recognized as a long‑time dividend grower, with analyses describing its dividend as both “stable” and “growing” over the past decade. [44]

A Barchart options‑focused article earlier this year highlighted that Chevron’s 4.6% dividend yield can be complemented by short‑put strategies that generate roughly 1.7% in additional one‑month premium income, underscoring CVX’s appeal to income‑oriented and options‑savvy investors. [45]

Is the dividend safe?

Third‑party dividend analytics, such as Simply Wall St, flag Chevron’s high earnings payout ratio as a potential risk, but note that cash‑flow coverage remains adequate and the company has ample flexibility via capex adjustments and buybacks. [46]

Given Chevron’s explicit commitment to capex and dividend breakeven below $50 Brent, management appears determined to defend the dividend, even through a period of softer oil prices — though that naturally raises the stakes of any prolonged downturn. [47]

Ownership, valuation and recent flows: what big money is doing

Institutional investors are still accumulating Chevron

Two new December 2 filings stand out:

- Brandes Investment Partners LP increased its CVX stake by 2.3% in Q2, now holding 687,909 shares worth about $98.5 million. [48]

- Beacon Pointe Advisors LLC boosted its CVX position by 10% in Q2, to 453,038 shares valued at roughly $64.9 million, making Chevron its 28th‑largest holding at about 0.7% of its portfolio. [49]

MarketBeat’s data show that around 72% of Chevron’s outstanding shares are held by hedge funds and other institutional investors, indicating strong “big money” participation. [50]

Insider activity

One notable insider move:

- Director John B. Hess (of Hess Corp fame) recently sold 275,000 Chevron shares at an average price of $150.75, cashing out around $41.5 million while still retaining over 1.12 million shares. [51]

While a large sale can spook some investors, it’s also typical for newly absorbed executives and directors to rebalance their holdings after a major merger.

Valuation snapshot

MarketBeat’s profile pegs Chevron at roughly: [52]

- Market cap: About $307 billion.

- P/E ratio: Around 19.6x trailing earnings.

- PEG ratio: About 4.4, indicating a higher valuation relative to expected growth.

- Beta: Roughly 0.83, suggesting less volatility than the market overall, despite oil‑price swings.

Other performance dashboards estimate a 10–11% annualized total return over the last decade, reflecting solid but not spectacular long‑term compounding when dividends are reinvested. [53]

Quant and technical forecasts: what the models say about CVX

Beyond Wall Street’s fundamental estimates, quantitative and technical models are also generating Chevron stock forecasts:

- CoinCodex’s algorithmic model expects CVX to rise toward about $157.34 by December 6, 2025, roughly 5% above current levels, and projects an average December 2025 price around $156.32 (about 6% higher than today). [54]

- The same model, however, flags “bearish” overall technical sentiment, noting that only one indicator is bullish versus 25 bearish, with just 14 green days in the last 30 trading days and a Fear‑mode reading on its Fear & Greed index. [55]

- Longer‑term, the CoinCodex forecast is aggressive, suggesting a one‑year target near $253.79 (around 66% upside) and a 2030 projection above $340, more than double today’s price — but the site clearly labels these as speculative technical projections rather than fundamental valuations. [56]

These quantitative tools can be interesting sentiment gauges, but they shouldn’t be treated as guarantees. Still, they reinforce the view that Chevron is in a consolidation phase, with many technical indicators flashing “Sell”, even as forecasting models tilt toward moderate price appreciation.

Chevron stock forecast for 2026 and beyond: tying it all together

Putting the various strands together, here’s how the Chevron (CVX) outlook currently stacks up.

1. Fundamental Street consensus (12–18 months)

- Price targets: Most broker price targets cluster between $165 and $175 per share, suggesting roughly 10–16% upside from today’s levels. [57]

- Dividend yield: Add in a 4.5–4.6% dividend yield, and the implied one‑year total return in a “base‑case” scenario lands somewhere in the mid‑teens to low‑20s percentage range, assuming targets are met. [58]

- Earnings path: Analysts expect 2025 EPS to dip meaningfully vs. 2024 due to lower oil prices and integration costs, then rebound in 2026 as synergies flow through and growth projects ramp up. TS2 Tech+1

2. Strategic drivers

Bullish forces:

- Record production boosted by Hess and the Tengiz expansion. [59]

- A clear 2030 plan with >10% annual FCF growth, 2–3% production growth, and strong buyback capacity at mid‑cycle oil prices. [60]

- High, growing dividend supported by robust cash flows and management’s commitment to shareholder returns. [61]

- New exploration options from Nigeria’s West Delta basin and other partnership‑driven plays. [62]

Bearish/uncertain forces:

- Oil‑price headwinds, with Chevron’s CFO herself expecting weakness possibly into 2026. [63]

- Geopolitical risk around the CPC pipeline and Kazakhstan volumes. [64]

- Hess integration risk, layoffs and political scrutiny of big‑oil mergers. [65]

- A high earnings payout ratio, which could become uncomfortable if oil spends a long time below management’s breakeven assumptions. [66]

3. What this means for different types of investors

- Income‑focused investors: Chevron remains one of the largest, most established dividend payers in the energy sector, with a yield well above the market, a long history of increases, and a management team explicitly managing the business around supporting that payout. [67]

- Growth‑oriented investors: The case hinges on execution — can Chevron deliver on its Hess synergies, Tengiz expansion, Nigeria and other exploration, while using technology and AI to cut costs and open new markets? [68]

- Macro‑sensitive traders: Near‑term moves in CVX will likely remain tightly linked to oil prices, CPC headlines and OPEC+ decisions, with technical models currently skewed bearish even as fundamental forecasts call for rebound. [69]

Key risks to watch

Even with today’s bullish headlines, Chevron is not a risk‑free story. The main pressure points include:

- Commodity price volatility

A prolonged period of Brent well below the $60–70 range could strain both dividends and buybacks, despite improved breakevens. [70] - Geopolitics in Kazakhstan and Russia

The CPC drone attack highlights just how exposed Chevron’s Kazakh barrels are to a single export route that runs through Russia. [71] - Hess integration and regulatory scrutiny

Hess adds fantastic assets but also integration complexity, layoffs and legal/political overhang, especially after a high‑profile Exxon dispute and increasing scrutiny of big‑oil consolidation. [72] - Restructuring, safety and social license

Workforce reductions and refinery incidents (such as the El Segundo refinery fire lawsuit) can affect community relations, regulatory risk and brand perception. [73] - Energy transition and policy shifts

Chevron is still overwhelmingly an oil‑and‑gas business at a time when climate policy and investor preferences are shifting. Faster‑than‑expected decarbonization policies could pressure its long‑term demand outlook, even as it invests in lower‑carbon projects and AI‑linked power solutions. [74]

Final thoughts: Is Chevron stock a buy right now?

On December 2, 2025, Chevron stock sits at an interesting crossroads:

- The income case is strong: a 4.5%+ yield, a long record of dividend growth, and explicit management targets built around sustaining that payout through the cycle. [75]

- The growth and value case depends on your belief that Chevron can:

- Navigate a soft oil market into 2026,

- Execute on its Hess integration and global expansion (Kazakhstan, Guyana, Nigeria, Permian), and

- Deliver on its 2030 promise of double‑digit free‑cash‑flow growth. [76]

Analyst targets suggest moderate upside over the next year, especially when combined with the dividend, but there are real macro and geopolitical risks that could derail the story.

If you’re considering Chevron today, it’s worth asking:

- How comfortable am I with oil‑price volatility and political risk?

- Is my time horizon long enough (5+ years) to ride through the integration and energy‑transition uncertainties?

- Do I value steady income more than fast capital gains?

As always, this article is not personal investment advice. Your decision on CVX should reflect your own risk tolerance, time horizon and portfolio goals, ideally with guidance from a qualified financial professional.

References

1. www.marketbeat.com, 2. portfolioslab.com, 3. portfolioslab.com, 4. www.gurufocus.com, 5. www.investing.com, 6. stockanalysis.com, 7. www.marketbeat.com, 8. www.reuters.com, 9. www.reuters.com, 10. www.benzinga.com, 11. www.reuters.com, 12. www.zacks.com, 13. www.reuters.com, 14. www.reuters.com, 15. www.reuters.com, 16. www.reuters.com, 17. www.reuters.com, 18. www.reuters.com, 19. www.investopedia.com, 20. www.tgs.com, 21. www.reuters.com, 22. www.reuters.com, 23. northdakotamonitor.com, 24. www.businesswire.com, 25. www.investing.com, 26. www.investing.com, 27. www.keyfactsenergy.com, 28. www.keyfactsenergy.com, 29. www.marketbeat.com, 30. www.marketbeat.com, 31. www.reuters.com, 32. www.reuters.com, 33. www.reuters.com, 34. www.reuters.com, 35. www.reuters.com, 36. www.reuters.com, 37. www.reuters.com, 38. www.reuters.com, 39. www.energy-reporters.com, 40. www.energy-reporters.com, 41. www.marketbeat.com, 42. www.dividend.com, 43. simplywall.st, 44. simplywall.st, 45. www.barchart.com, 46. simplywall.st, 47. www.reuters.com, 48. www.marketbeat.com, 49. www.marketbeat.com, 50. www.marketbeat.com, 51. www.marketbeat.com, 52. www.marketbeat.com, 53. www.financecharts.com, 54. coincodex.com, 55. coincodex.com, 56. coincodex.com, 57. stockanalysis.com, 58. www.dividend.com, 59. www.keyfactsenergy.com, 60. www.reuters.com, 61. simplywall.st, 62. www.reuters.com, 63. www.energy-reporters.com, 64. www.reuters.com, 65. www.reuters.com, 66. simplywall.st, 67. www.chartmill.com, 68. www.reuters.com, 69. www.energy-reporters.com, 70. www.reuters.com, 71. www.reuters.com, 72. www.investopedia.com, 73. simplywall.st, 74. www.reuters.com, 75. www.dividend.com, 76. www.reuters.com

Stock After Hours Today (Dec. 22, 2025): Latest News, Analyst Forecasts, and What to Watch Before Tuesday’s Open")

: What to Watch Before Tuesday’s Market Open — GDP Data, AI Catalysts, and Key Levels")

Stock After Hours Today (Dec. 22, 2025): Closing Price, Nasdaq-100 Effect, Fresh Forecasts, and What to Watch Before Tuesday’s Open")

Stock on December 2, 2025: West Qurna Deal Talks, Hydrogen Pivot and 2026 Price Targets")

on December 2, 2025: Earnings Power, Institutional Buying and Robotaxis Drive the 2026 Outlook")