Date: December 1, 2025

Chevron Corporation (NYSE: CVX) is back in the spotlight to start December, as a fresh analyst upgrade, a high‑profile drone attack on a key export terminal and the company’s ambitious 2030 free‑cash‑flow plan all hit the tape at once.

As of the latest trading on Monday, Chevron stock is changing hands around $152–153 per share, giving the U.S. supermajor a market capitalization of roughly $300 billion. [1] Year to date, CVX has delivered a total return of about 10.6%, while offering an annualized dividend of $6.84 per share, a forward yield of roughly 4.5%—above its five‑year average yield near 4.1%. [2]

Below is a rundown of the latest Chevron stock news, forecasts and analysis as of December 1, 2025, and what it all means for CVX investors.

Chevron stock price snapshot: income-heavy, mid‑range in its 52‑week band

At today’s levels, Chevron trades:

- Around $152–153 per share, slightly above recent closes. [3]

- Within a 52‑week range of about $132.04 to $168.96, roughly the middle of that band. [4]

- On a forward P/E multiple in the high‑teens to ~20×, depending on the earnings estimate set used. [5]

Income remains the key attraction: Chevron’s $1.71 quarterly dividend (next payable on December 10) equates to a 4.4–4.6% yield at current prices, and the company has increased its annual payout for 38 consecutive years. [6] One recent analysis notes that today’s yield sits above the stock’s five‑year average of ~4.08%, a classic sign that income investors may be getting paid a bit extra for taking on energy‑sector cyclicality right now. [7]

Fresh December 1 headlines: analyst upgrades and geopolitical tension

HSBC upgrade: “share weakness overdone”

The headline move for December 1, 2025 is an upgrade from HSBC:

- HSBC analyst Kim Fustier upgraded Chevron from Hold to Buy (some databases show this as Hold → Strong Buy) and

- Raised the 12‑month price target from $166 to $169, implying roughly 11% upside from around $152.5. [8]

Coverage from GuruFocus, MarketScreener, Fintel and others highlights that HSBC views Chevron’s recent share weakness as overdone, pointing to the company’s strong balance sheet, resilient free cash flow and multi‑year growth runway from Guyana, Kazakhstan and the Permian Basin. [9]

Chevron also lands on multiple “top upgrades” lists today, including Benzinga’s rundown of Monday’s top five stock upgrades and 24/7 Wall St.’s compilation of the day’s key research calls, both of which spotlight the HSBC move on CVX. [10]

UBS, RBC, Mizuho and others reinforce a bullish tilt

HSBC isn’t alone. Several major houses have recently reiterated or raised positive views on Chevron, and those notes are being re‑circulated in Monday’s coverage:

- UBS reiterated a Buy rating and set a $197 price target, citing strong free cash flow and confidence in Chevron’s post‑Hess strategy. [11]

- RBC Capital Markets maintained an Outperform rating with a $175 target, arguing that the Investor Day plan de‑risks Chevron’s growth trajectory. [12]

- Mizuho recently nudged its target up from $191 to $204 while keeping an Outperform/Buy view. [13]

- Piper Sandler continues to rate Chevron Overweight/Buy, trimming its target only slightly from $169 to $168. [14]

- Morgan Stanley maintained an Overweight rating in early November, with an analyst forecast that implies roughly 12% upside. [15]

Taken together, the marginal analyst moves are skewing more bullish, even as some legacy “Sell” and “Hold” ratings keep the formal consensus below a full‑throated Strong Buy.

CPC drone attack: risk reminder, but exports continue

The other big Chevron‑linked story this weekend was a Ukrainian naval drone attack on the Caspian Pipeline Consortium (CPC) terminal at Novorossiysk, Russia, the export route for oil from Kazakhstan’s giant Tengiz field, where Chevron owns 50% of the Tengizchevroil (TCO) venture. [16]

Key points from today’s updates:

- On November 29, a drone strike severely damaged Single‑Point Mooring (SPM) 2, temporarily halting operations at the Black Sea terminal. [17]

- Analysts estimate CPC exports were roughly halved immediately after the attack. [18]

- CPC and Chevron now say oil loadings have resumed via SPM 1, while SPM 3 had already been under repair since mid‑November and may take up to two months to restore. [19]

- Overall, CPC still handles more than 1% of global oil supply, underscoring how exposed Chevron’s Kazakh barrels are to this corridor. [20]

Chevron has confirmed that crude liftings from its Tengizchevroil project are continuing despite the damage, and satellite and shipping data cited in the reports show activity resuming from at least one mooring point. [21]

For investors, the near‑term takeaway is that cash flow from Tengiz is still flowing, but the incident is a stark reminder that part of Chevron’s growth story hinges on infrastructure located close to a live war zone.

Portfolio moves and ownership shifts

Recent lesser‑known but still relevant items:

- TotalEnergies has agreed to sell a 40% stake in two Nigerian offshore blocks (PPL 2000 and PPL 2001) to Chevron, expanding Chevron’s West African footprint; detailed terms remain behind paywalls but the deal underscores the company’s push for long‑life offshore resources. [22]

- Several institutional investors have reported new or increased positions in Chevron in recent 13F‑style filings, including Sepio Capital LP, Smith Moore & Co. and Leuthold Group LLC, which disclosed a new stake of 2,559 CVX shares. [23]

- A separate November piece highlighted Warren Buffett’s Berkshire Hathaway as continuing to hold Chevron among its energy exposures, even as Berkshire has been a net seller of stocks overall, reinforcing CVX’s status as a “Buffett name” many investors follow closely. [24]

Q3 2025: record production, earnings beat and Hess integration noise

Chevron’s latest financial anchor is its third‑quarter 2025 report, released at the end of October:

- Reported earnings:$3.5 billion, or $1.82 per diluted share, versus $4.5 billion a year earlier. [25]

- Adjusted earnings: about $3.6 billion, or $1.85 per share, after excluding roughly $235 million of special items, largely severance and Hess transaction costs. [26]

- Revenue: in the high‑$40‑billion range, beating Wall Street expectations by more than $1 billion. [27]

- Production: a record 4.1 million barrels of oil equivalent per day (boe/d), up 21% year on year, driven largely by the Hess acquisition and ramp‑ups in the Permian and Kazakhstan. [28]

On the earnings call, management emphasized that while GAAP profit is being weighed down in the near term by integration and restructuring charges, the underlying cash‑generation engine remains robust. That view is backed up by the earnings surprise: adjusted EPS of $1.85 versus consensus of around $1.75, and revenue that handily topped forecasts. [29]

The Hess deal, completed in July, is clearly visible in these numbers:

- Chevron has said the acquisition will add roughly 450,000–500,000 boe/d in the near term and has already helped lift global production from 3.4 million boe/d in Q2 to 4.1 million in Q3. [30]

- However, management also guided to a $200–$400 million hit to Q3 earnings related to the deal, plus an additional $1.0–$1.25 billion in capital spending for the quarter as Hess is integrated into the portfolio. [31]

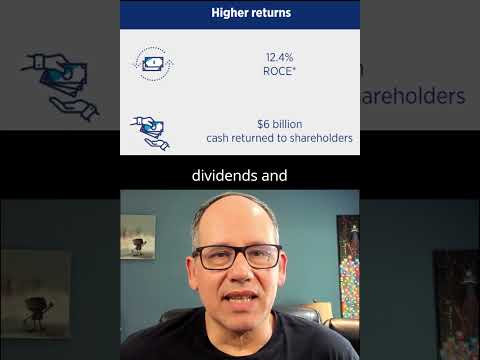

Longer term, Chevron is targeting at least $1 billion in annual cost synergies and a sustained double‑digit Return on Capital Employed (ROCE) at mid‑cycle oil prices from the combined Chevron‑Hess portfolio. [32]

Strategy reset: Investor Day 2025 and the 2030 roadmap

Chevron’s November 12 Investor Day in New York provided the clearest picture yet of how management sees the post‑Hess company through 2030.

According to the company and Reuters coverage, Chevron now aims to: [33]

- Grow free cash flow and earnings per share by more than 10% annually through 2030, assuming $70 Brent.

- Deliver 2–3% annual oil and gas production growth, off the new ~4.1 million boe/d base.

- Lower annual capital expenditure guidance to $18–21 billion, down from the prior $19–22 billion range.

- Increase cost‑reduction targets to $3–4 billion by the end of 2026, up from a previous $2–3 billion.

- Maintain a capex + dividend breakeven below $50 Brent through 2030.

- Return $10–20 billion per year in share buybacks from 2026 onward, subject to commodity conditions. [34]

The cost savings will come from a combination of upstream divestments, headcount reductions (up to 20% of the workforce, or about 8,000 jobs) and technology‑driven efficiency, including more remote operations. [35] That program has already led to more than 100 layoffs in North Dakota following the Hess merger and is reshaping Chevron’s footprint in several regions. [36]

At the same time, Chevron is leaning into large, long‑life projects:

- The $48 billion Tengiz expansion in Kazakhstan is coming online, with capacity expected to reach about 1 million boe/d—roughly 1% of global crude supply—and projected to generate around $4 billion in free cash flow in 2025, rising to $5 billion in 2026 at $60 Brent. [37]

- The completed Hess acquisition gives Chevron a coveted 30% stake in Guyana’s Stabroek block, one of the most prolific oil discoveries of recent decades, plus additional scale in the Bakken shale. [38]

- In the U.S. Gulf of Mexico, Chevron’s Anchor project is part of a broader revival in deep‑sea drilling, enabled by high‑pressure technology that can tap previously inaccessible reservoirs—though not without environmental and political scrutiny. [39]

Investor reaction to the Investor Day has been broadly positive. UBS, RBC, Goldman Sachs and others have pointed to the plan as evidence that Chevron can grow volumes and shrink its cost base while still returning substantial cash to shareholders, even if oil prices drift lower from current levels. [40]

Chevron dividend, payout ratio and valuation

Dividend profile

By the numbers:

- Current quarterly dividend: $1.71 per share. [41]

- Annualized: $6.84, for a 4.4–4.6% yield at current prices. [42]

- Ex‑dividend date for the upcoming payment: November 18, 2025; payable December 10, 2025. [43]

- 1‑year dividend growth: roughly 4.9%, continuing nearly four decades of annual hikes. [44]

The flip side is a temporarily high payout ratio: MarketBeat and other sources peg Chevron’s dividend payout at roughly 96% of current‑year earnings, reflecting a year in which EPS has compressed much faster than the dividend. [45]

Management’s 10%+ free‑cash‑flow growth target through 2030, however, is explicitly designed to bring that payout ratio back down over time, while keeping the dividend growing and buybacks meaningful. [46]

Valuation snapshot

Different data providers show slightly different numbers, but the overall picture is consistent:

- Forward P/E: around 18–20× expected 2025 EPS. [47]

- Price‑to‑sales: about 1.6× trailing twelve‑month revenue. [48]

- Net profit margin: approximately 6–7%. [49]

On a yield basis, Chevron looks slightly cheap to its own history, with today’s 4.5%+ dividend yield sitting above the long‑run average. [50] On an earnings multiple basis, it trades at a premium to some integrated peers but a discount to many high‑growth sectors, reflecting its relatively stable but cyclical cash flows.

CVX stock forecast: what Wall Street expects now

If you aggregate the major analyst and data platforms, a fairly tight band of outcomes emerges for the next 12 months:

- MarketBeat (23 brokerages): consensus rating “Hold”, with 3 Sell / 9 Hold / 11 Buy and an average 1‑year price target of about $166.55—roughly 9% upside from current prices. [51]

- StockAnalysis (16 analysts): consensus “Buy”, average target $172.13, implying about 13% upside, with targets spanning $124–$204. [52]

- GuruFocus (23 analysts): average target around $172.4 (≈14% upside), but its internal “GF Value” model pegs one‑year fair value nearer $142.7, suggesting the stock trades somewhat above its proprietary fair‑value line. [53]

- TickerNerd (40 analysts): overall bullish stance with a median price target of $171, a range of $124–$197, and roughly 13% implied upside along with a Buy‑leaning mix of 15 Buys, 11 Holds and 1 Sell. [54]

- ValueInvesting.io (32 analysts): average target $175.83, about 16% upside, but with an overall Hold recommendation, reflecting the split between bulls and skeptics. [55]

- Benzinga’s November review likewise characterizes Chevron as a consensus Buy with a $173 target, a high target near $201 and a low around $124. [56]

Looking beyond the headline targets, StockAnalysis shows analysts expecting: [57]

- 2025 EPS to fall about 24% year over year (to roughly $7.38), as oil prices normalize and Hess integration costs hit, and

- 2026 EPS to rebound by ~11% to around $8.17, with revenue growth of about 3.7%.

In other words, the Street largely sees 2025 as a “transition” year for Chevron: earnings dip, capex and integration costs stay elevated, but volume growth and cost cuts lay the foundation for stronger earnings and cash flow thereafter.

Key risks CVX investors should watch

Even with today’s bullish headlines, Chevron is not a risk‑free story. The major pressure points include:

- Commodity price volatility

Chevron’s cash flows remain heavily tied to oil and gas prices. The company’s breakeven levels have improved, but a prolonged period of Brent well below the $60–70 range would still stress both the dividend and the buyback plan. - Geopolitical risk in Kazakhstan and Russia

The CPC drone attack illustrates the vulnerability of Chevron’s Kazakh barrels to the Caspian Pipeline Consortium, which traverses Russian territory to the Black Sea. Chevron leads Tengizchevroil with a 50% stake, and both Tengiz and CPC are central to its growth and free‑cash‑flow plans. [58] - Hess integration and regulatory overhang

While the Federal Trade Commission in July reopened and set aside its prior consent order limiting John Hess’s role on Chevron’s board—explicitly stating that the complaint had not pled an antitrust violation—future political scrutiny of oil mergers remains a real possibility. [59] Operationally, Chevron still has to deliver on its promised Hess synergies without major execution missteps. - Restructuring, safety and social license

Chevron is cutting up to 20% of its global workforce, including more than 100 jobs in North Dakota tied to the Hess merger, and is still dealing with the aftermath of a large fire at its El Segundo refinery in California. [60] Aggressive cost cutting can boost margins, but it also raises questions about safety, regulatory scrutiny and community relations. - Energy transition and policy shifts

Chevron is investing in lower‑carbon businesses and even planning a gas‑fueled AI data center in West Texas, but it remains overwhelmingly an oil‑and‑gas company at a time when policy and investor preferences are shifting. [61] Faster‑than‑expected policy changes—or a sharp deterioration in fossil‑fuel demand—could challenge the longer‑term 2030 plan.

Bottom line: what today’s news means for Chevron stock

Putting it all together:

- Near term, CVX is supported by:

- A 4.5%+ dividend yield,

- Fresh bullish signals from HSBC, UBS, RBC, Mizuho and others, and

- Reassurances that Kazakh exports are still flowing after the CPC drone attack. [62]

- Medium term (2025–2026), the Hess integration, Tengiz ramp‑up and cost‑cutting program are likely to make earnings somewhat noisy, but Wall Street largely expects EPS to trough in 2025 and reaccelerate in 2026, with mid‑single‑digit production growth and double‑digit free‑cash‑flow growth if management hits its Investor Day targets. [63]

- Over a 12‑month horizon, the bulk of analyst targets cluster in the mid‑$160s to mid‑$170s, implying roughly 9–16% price upside on top of the 4–5% dividend yield, albeit with some dissenting “Sell” ratings and fair‑value models that suggest the stock is already close to fairly valued. [64]

For investors and traders watching CVX today, the message from the market is fairly clear: Chevron is an income‑rich, mega‑cap energy name with a credible growth and efficiency plan—but also very real geopolitical and cyclical risks.

As always, this overview is informational only and not investment advice. Anyone considering Chevron stock should weigh their own risk tolerance, time horizon and views on global oil demand, and, ideally, consult a qualified financial adviser.

References

1. www.marketbeat.com, 2. finance.yahoo.com, 3. www.marketbeat.com, 4. www.dividend.com, 5. www.dividend.com, 6. www.dividendmax.com, 7. kalmbachmarkets.com, 8. www.gurufocus.com, 9. www.gurufocus.com, 10. www.benzinga.com, 11. www.investing.com, 12. www.investing.com, 13. www.gurufocus.com, 14. www.gurufocus.com, 15. fintel.io, 16. www.chevron.com, 17. www.reuters.com, 18. www.reuters.com, 19. www.reuters.com, 20. www.reuters.com, 21. www.reuters.com, 22. www.inkl.com, 23. www.marketbeat.com, 24. 247wallst.com, 25. chevroncorp.gcs-web.com, 26. www.chevron.com, 27. www.investing.com, 28. chevroncorp.gcs-web.com, 29. www.investing.com, 30. www.reuters.com, 31. www.reuters.com, 32. www.chevron.com, 33. www.reuters.com, 34. finance.yahoo.com, 35. www.reuters.com, 36. northdakotamonitor.com, 37. www.reuters.com, 38. www.reuters.com, 39. www.ft.com, 40. www.investing.com, 41. www.chevron.com, 42. www.dividend.com, 43. www.dividendmax.com, 44. stockanalysis.com, 45. www.marketbeat.com, 46. www.reuters.com, 47. www.dividend.com, 48. tickernerd.com, 49. tickernerd.com, 50. kalmbachmarkets.com, 51. www.marketbeat.com, 52. stockanalysis.com, 53. www.gurufocus.com, 54. tickernerd.com, 55. valueinvesting.io, 56. www.benzinga.com, 57. stockanalysis.com, 58. www.reuters.com, 59. www.ftc.gov, 60. www.reuters.com, 61. www.reuters.com, 62. www.gurufocus.com, 63. stockanalysis.com, 64. www.marketbeat.com

Stock on Dec 22, 2025: ₹3,300-Crore Bond Deal Draws Big NBFC Money as AGR Relief Hopes Build")

")

: Stock Rises as Rights Issue Call, Leadership Rejig and Tariff-Hike Bets Drive Fresh Focus")

Stock Outlook for December 2025: Dividend Hike, Q3 Earnings Beat and Rising Analyst Targets")

Stock Near Record Highs Ahead of Q4 2025 Earnings: Buy, Hold or Take Profits?")